1. はじめに ・ エグゼクティブサマリー / Foreword & Executive Summary

平素より格別のご支援を賜り、誠にありがとうございます。

Thank you always for your continued support. This is TK, representative of EX Group.

本号は2026年5月の一ヶ月間の動向を総括するレポートとして発行しております。月次レポートとして、ドバイ政府の月次データ確定後に月初め約一週間以内を目途に発行してまいります。本レポートは事実と出典のみを整理し、弊社の判断や予測は収録しておりません。

This issue is published as a comprehensive monthly review covering one month of developments. Monthly reports are published within five days of the end of each month after DLD monthly data is finalized. This report contains only verified facts and sourced citations; EX Group business decisions and forecasts are not included.

- 米中サミット実施(5/14)と米イラン和平交渉のMOU到達(5/28)

US-China summit (May 14) and the MOU breakthrough in US-Iran peace negotiations (May 28). - レバノン情勢の継続(5/28ベイルート空爆、5/30 Kiryat Shmonaへのロケット攻撃)Lebanon situation continued (May 28 Beirut strikes, May 30 Kiryat Shmona rocket attack).

- 原油3指標(WTI/Brent/Dubai現物)が収斂、4月時点の各社予想を下回る水準で推移Three crude benchmarks (WTI/Brent/Dubai spot) converged below April forecasts.

- ドバイ不動産取引量(総取引額は戦前の約半分に)

取引:10,483件 / AED 29.46B(前月比▼25.6% / ▼39.2%、2月戦前比▼38.4% / ▼51.5%)

Dubai Real Estate / DLD May transactions: 10,483 / AED 29.46B (▼25.6% / ▼39.2% MoM; ▼38.4% / ▼51.5% vs February pre-conflict). - ハッジ2026最終巡礼者数1,707,301人(前年+34,071人)、戦時下にもかかわらず前年比増(GASTAT発表) *ハッジはイスラム教の重要なイベントです。

Hajj 2026 final pilgrim count: 1,707,301 (+34,071 YoY), increased year-on-year despite wartime (GASTAT). - サウジ外国人不動産所有法2026年1月施行、6月にトークン化制度の本格展開予定

Saudi foreign property ownership law in effect since January 2026; tokenization regulation expected in June. - 飲食業界は売上低下が継続、価格交渉局面に変化の兆し。倒産関連は政府救済策により表面化が抑制されている状況

F&B sector sales decline continues with shifting negotiation phase. Insolvency surface suppressed by government relief measures.

- 5月1日:UAEのOPEC脱退発効

May 1: UAE OPEC withdrawal takes effect. - 5月14-15日:トランプ大統領訪中、習近平国家主席と首脳会談

May 14-15: Trump’s state visit to Beijing, summit with President Xi. - 5月14日:米中共同声明発表(ホルムズ海峡・イラン核問題)

May 14: US-China joint statement on Hormuz and Iran nuclear issue. - 5月25-30日:ハッジ2026(メッカ巡礼)

May 25-30: Hajj 2026 pilgrimage period. - 5月26日:アラファの日 / 5月27日:Eid al-Adha

May 26: Day of Arafah / May 27: Eid al-Adha. - 5月27日:トランプ大統領、キャンプ・デービッドで閣議招集

May 27: Trump convenes cabinet at Camp David. - 5月28日:米イラン暫定MOU到達と報道、同日米軍がイラン拠点攻撃

May 28: US-Iran interim MOU reported; US military strikes Iranian sites same day. - 5月29日:GASTAT、ハッジ2026最終巡礼者数1,707,301人を発表

May 29: GASTAT announces Hajj 2026 final count of 1,707,301 pilgrims.

2. 軍事・外交情勢 / Military & Diplomatic Update

2-1. 5月の全体構造 / Overall Structure in May

5月の中東情勢は、終戦交渉が本格化する一方、軍事行動が並行して継続するという二重構造で推移しました。終戦交渉は米イラン間の暫定MOU到達まで進展した一方、イスラエルとヒズボラの戦闘はレバノンで別トラックにおいて継続しています。

The Middle East situation in May 2026 unfolded under a dual structure: peace negotiations advanced significantly while military operations continued in parallel. US-Iran negotiations reached an interim MOU breakthrough, while the Israel-Hezbollah conflict in Lebanon continued a separate track.

2-2. 米中首脳会談(5月14-15日) / US-China Summit (May 14-15)

トランプ大統領が約10年ぶりに現職米大統領として中国を訪問し、習近平国家主席と会談を実施。会談の評価(成果)について、米国主要メディアの論調は二つに分かれています。

President Trump made the first state visit to China by a sitting US president in approximately a decade. US major media coverage of the summit divided into two distinct narratives.

両者は以下の事項で合意したとホワイトハウスが公表しています。

The White House announced agreement on the following items:

- 「イランが核兵器を取得することは認められない」

‘Iran cannot be permitted to acquire nuclear weapons.’ - 「世界のエネルギー流通を確保するためホルムズ海峡が開かれ続けねばならない」

‘The Strait of Hormuz must remain open to ensure global energy flow.’ - 習近平国家主席はホルムズ海峡の軍事化に反対、米国産原油の追加購入に関心を表明

President Xi opposed militarization of Hormuz and expressed interest in additional US crude oil purchases. - 経済協力の拡大、米国企業の市場アクセス、中国による米国産農産物購入の増加、フェンタニル対策

Expanded economic cooperation, market access for US companies, increased Chinese purchases of US agricultural products, and fentanyl precursor measures.

- 習近平国家主席は会談を「歴史的」「画期的」と評価

President Xi characterized the meeting as ‘historic’ and ‘epoch-making.’ - 両者は「経済貿易関係の安定維持、各分野での実務協力の拡大、双方の懸念への適切な対応について重要な共通理解に達した」

Both reached ‘important common understandings on maintaining stable economic and trade relations, expanding practical cooperation, and properly handling each other’s concerns.’ - 「中東情勢を含む主要な国際・地域問題について見解を交換した」

‘Exchanged views on major international and regional issues including the Middle East situation.’ - 習近平国家主席の秋の訪米(9月24日予定)を確認

President Xi’s autumn visit to the US (scheduled September 24) confirmed.

両国の公式発表には言及項目の違いが見られます。米国側の発表には台湾への言及がなかった一方、中国側リードアウトにはイランへの言及がなかった。台湾について、習近平国家主席はトランプ大統領に対し、台湾問題が「適切に処理されない」場合、両国は「衝突、さらには紛争を起こし、関係全体を大きな危険にさらす」と警告したと報じられています。

Official statements from both sides showed differences in items referenced. The US readout omitted any mention of Taiwan, while the Chinese readout omitted Iran. On Taiwan, President Xi reportedly warned President Trump that if the Taiwan issue is ‘not properly handled,’ the two countries could ‘fall into conflict, even confrontation, putting the entire relationship at great risk.’

米メディアは、大きく2つの論調に分かれ、この評価が注目を集めました。

【「成果が限定的だった」とする論調】 Narrative: ‘Limited outcomes’

トランプは求めていた華やかさを手に入れた。しかし米大統領は始まった時とほぼ同じ場所で首脳会談を終えた。自称『友人』である習からは、イランでの混乱した戦争への対処や、国内の困難な政治情勢に対して、ほとんど助けを得られなかった

— Bloomberg, May 15, 2026

米国と中国は、北京サミットで議論されたイランや台湾などの問題について、いかなる重要な進展も発表しなかった

— NBC News, May 15, 2026

CSIS(戦略国際問題研究所)は「世界で最も重要な二国間関係における安定性と予測可能性に向けた比較的控えめな一歩」と評価しています。

CSIS assessed the summit as ‘a relatively modest step toward stability and predictability in the world’s most important bilateral relationship.’

【「トランプ大統領が大きな成果を得た」とする論調】 Narrative: ‘Trump achieved major outcomes’

トランプ大統領は習近平国家主席が高度な北京会談に続いてイランとの取引を仲介しホルムズ海峡を再開するための支援を申し出たことを明らかにした

— Fox News, May 14, 2026

トランプ大統領のメディア・インタビューでは、習近平国家主席が「私が何かの役に立てるなら、お手伝いしたい」と述べ、ホルムズ海峡が開かれることを望み、イランに軍事装備を提供しないと確約したと報じられています(中国側公式発表での確認はされていません)。

President Trump’s media interviews reported that President Xi stated ‘if I can be of help on anything, I want to help,’ and pledged not to provide military equipment to Iran (not confirmed in the Chinese official readout).

2-3. 米イラン和平交渉の進展 / Progress in US-Iran Peace Negotiations

5月後半、米イラン間の交渉はパキスタン仲介のもと、ドーハ(カタール)を主な舞台として進展しました。

In the latter half of May, US-Iran negotiations advanced primarily in Doha (Qatar) under Pakistani mediation.

複数報道によれば、米イラン両国は既存の停戦をより恒久的な合意へと転換する暫定的なMOU(覚書)に到達したとされています。

According to multiple reports, the US and Iran reached an interim MOU to convert the existing ceasefire into a more permanent agreement.

- ホルムズ海峡の航行を第一歩の合意とする

Navigation through the Strait of Hormuz set as the first-step agreement. - MOU署名後にイランの核計画について60日間の交渉期間を開始

A 60-day negotiation period on Iran’s nuclear program begins upon MOU signing. - 合意が成立すれば、240億ドル相当のイラン凍結資産が解放される可能性。米政府高官はCNNに対し、資産凍結解除はホルムズ海峡再開後と発言

If finalized, approximately $24B in frozen Iranian assets could be released. US official told CNN that asset release would only follow Hormuz reopening.

【1. 濃縮ウランの扱い】 Treatment of Enriched Uranium

我々はそれを必要としないし、欲しくもない。手に入れたら恐らく破壊するが、彼らに持たせはしない

— トランプ大統領発言(5月21日) / President Trump, May 21, 2026

これに対しイラン側は、米国のウラン引き渡し要求は合意を破綻させると表明しています。

Iran responded that US demands for uranium handover would break the agreement.

【2. ホルムズ海峡の管理権】 Control of the Strait of Hormuz

ルビオ国務長官は5月21日、合意が視野に入る「良い兆候」があると述べる一方、イランがホルムズ海峡の航行を恒久的に支配する措置を追求すれば、いかなる合意も「実現不可能」になると警告。「通行料制度を支持する者は世界に誰もいない」と発言したと報じられています。

Secretary Rubio noted ‘good signs’ that an agreement was in sight but warned on May 21 that if Iran sought permanent control over Hormuz navigation, any agreement would be ‘unworkable.’ He reportedly said ‘no one in the world supports a transit fee system.’

- 5月25-26日:米軍がホルムズ海峡周辺のイランの無人機発射拠点とボートを攻撃

May 25-26: US military strikes Iranian drone launch sites and boats around the Strait of Hormuz. - 5月28日早朝:米軍がイラン側施設を攻撃。同日、テヘランも反撃を警告、クウェートの米軍基地方向への発砲も報じられている

May 28 early morning: US military strikes Iranian facilities. Tehran warned of counterattack same day; firing toward US base in Kuwait was reported. - 5月27日:トランプ大統領はキャンプ・デービッドで閣議を招集、シチュエーションルームでイラン政策の次のステップを検討

May 27: President Trump convened cabinet at Camp David and reviewed next steps in Iran policy in the Situation Room.

2-4. レバノン情勢 / Lebanon Situation

イスラエルとヒズボラの戦闘は、米イラン交渉の枠外で継続しています。イスラエル側は4月の停戦時から「停戦はヒズボラとの戦争には及ばない」との立場を維持しており、レバノンでの作戦は米イラン交渉とは別枠で扱われています。

Hostilities between Israel and Hezbollah continued outside the framework of US-Iran negotiations. Israel has maintained its position since the April ceasefire that ‘the ceasefire does not extend to the war with Hezbollah,’ with Lebanon operations treated separately from US-Iran talks.

- 5月28日:イスラエル軍がベイルート南部を3週間ぶりに空爆。レバノン保健省は少なくとも19人死亡、58人負傷と発表

May 28: Israeli airstrikes on southern Beirut for the first time in three weeks. Lebanon’s Ministry of Health reported at least 19 killed and 58 wounded. - 5月30日:ヒズボラが北部Kiryat Shmonaにロケット攻撃

May 30: Hezbollah strikes northern Kiryat Shmona with rockets. - 過去1週間で、イスラエルの攻勢は1日平均11人の子供を殺害または負傷させたと国連児童機関(UNICEF)が発表

Over the past week, Israeli offensives killed or injured an average of 11 children per day, UNICEF reported. - ルビオ国務長官は5月29日、レバノンのアウン大統領と電話会談、停戦合意の必要性を協議

Secretary Rubio held a phone call with Lebanese President Aoun on May 29, discussing the need for a ceasefire.

2-5. 周辺国の動向 / Regional Actors

- 駐米大使「単なる停戦では不十分」「ホルムズ海峡の無条件再開、イランの賠償責任、地域での武装勢力支援を縮小する広範な合意」を要求

UAE Ambassador to US: ‘Ceasefire alone is insufficient.’ Demands ‘unconditional reopening of Hormuz, Iranian responsibility for damages, and broad agreement to reduce regional proxy support.’ - UAEはサウジ・カタールとともに、トランプ大統領に「(和平交渉に)チャンスを与えるよう」呼びかけた

UAE, alongside Saudi Arabia and Qatar, called on President Trump to ‘give peace negotiations a chance.’ - 5月、ワルツ米国連大使がUAEはイスラエル製アイアンドーム迎撃システムを受領し、入ってくるイランミサイルの撃墜に使用したと確認

In May, US UN Ambassador Waltz confirmed that UAE received Israeli-made Iron Dome interceptor systems and used them to shoot down incoming Iranian missiles. - NYTは、UAEがイランのラヴァン島の製油所等への報復攻撃を実施したと報道

The New York Times reported that UAE conducted retaliatory strikes on Iran’s Lavan Island refinery and other targets.

- サウジの優先事項は交渉支持、最低目標はホルムズ海峡再開と直接攻撃への保証取り付け

Saudi Arabia’s priority is supporting negotiations; minimum objectives are Hormuz reopening and security assurances against direct attacks. - 4月8日にイランが湾岸エネルギーインフラを攻撃した際、サウジ油田と紅海ヤンブー・ターミナルを結ぶPetrolineが攻撃を受けた(紛争開始以来、石油インフラへの最大の協調攻撃)

Saudi oil fields and the Petroline pipeline connecting them to the Red Sea Yanbu Terminal were attacked during Iran’s April 8 strikes on Gulf energy infrastructure (largest coordinated attack on oil infrastructure since the conflict began). - 2025年9月の相互防衛協定に基づき、停戦後にパキスタンが13,000人の部隊と戦闘機をサウジに派遣

Under the September 2025 mutual defense agreement, Pakistan deployed 13,000 troops and fighter jets to Saudi Arabia after the ceasefire.

- カタール:イランの首席交渉官と外相がドーハを訪れ、カタール首相と米国との潜在合意について協議

Qatar: Iran’s chief negotiator and foreign minister visited Doha to discuss potential US agreement with Qatari PM. - オマーン:アラブ湾岸国で唯一、米・イスラエルの攻撃を直接批判。ホルムズ海峡再開の運用について、イラン側はオマーンとプロトコル合意の下で航行サービスを実施すると表明

Oman: Only Arab Gulf state directly criticizing US-Israeli strikes. Iran stated Hormuz reopening operations would be conducted under a protocol agreement with Oman. - イラク:湾岸諸国は、地域で攻撃を行ってきたイラン支援の民兵をイラク政府がより良く統制するよう求めている

Iraq: Gulf states are calling on the Iraqi government to better control Iranian-backed militias that have conducted regional attacks.

2-6. 全体構図 — 3つの独立トラック / Overall Structure — Three Independent Tracks

5月時点で、戦闘は概ね三つの独立したトラックで進行しています。

As of May, hostilities are proceeding broadly on three independent tracks.

| トラック / Track | 状態 / Status | 5月の動き / May Developments |

|---|---|---|

| 米国-イラン本線 | 暫定MOU到達後の詰め交渉 | 5/28 暫定MOU、その後追加要求で停滞 |

| 米国-イラン軍事 | 海上封鎖継続、散発的攻撃 | 5/25-28 米軍がイラン拠点攻撃 |

| イスラエル-レバノン | 別枠で戦闘継続 | 5/28 ベイルート空爆、5/30 Kiryat Shmonaロケット |

3. エネルギー価格とOPEC関連 / Energy Prices & OPEC

3-1. 5月の原油価格動向 / Crude Oil Price Movement in May

5月の原油価格は、和平交渉の進展を反映して大幅に下落しました。月初の水準から月末にかけて、3つの主要ベンチマークいずれも約16〜19%の下落となっています。さらに4月のピーク水準比では約20%の低下となり、月次の下落幅としてはコロナ禍以来最大と報じられています。

Crude prices declined substantially in May, reflecting peace negotiation progress. All three major benchmarks fell approximately 16-19% from early to late May. Prices are also down roughly 20% from the April 2026 peak — reportedly the largest monthly decline since the COVID-19 pandemic.

- Brent:5月初 約$114 → 5月末 $92.56(▼約19%)

Brent: Early May ~$114 → End May $92.56 (▼~19%). - WTI:5月初 約$104 → 5月末 $87.18(▼約16.5%)

WTI: Early May ~$104 → End May $87.18 (▼~16.5%). - Dubai/Oman現物:4月ピーク $130-$150 → 5月末 約$95-100(▼約25-30%)

Dubai/Oman spot: April peak $130-$150 → End May ~$95-100 (▼~25-30%).

戦争のピーク時(3月後半〜4月初旬)には、現物原油ベンチマークと先物の間に$30〜$50/バレルの大きな乖離が見られました。和平交渉の進展と協調的戦略備蓄放出により、5月末時点では3指標の乖離は大幅に縮小しています。

During the war’s peak (late March-early April), spot crude benchmarks diverged from futures by $30-$50/bbl. With peace progress and coordinated SPR releases, the three-benchmark gap narrowed significantly by end-May.

3-2. 4月時点の各社予想との比較 / Comparison with April Forecasts

5月末の価格水準は、4月時点で主要機関が示していた見通しと比較して、いずれの予想からも低い水準で推移しています。

End-May prices trended below the forecasts presented by major institutions as of April.

| 機関 / Institution | ベンチマーク | 2026年想定価格 | 5月末との乖離 |

|---|---|---|---|

| Goldman Sachs | Brent | 2026年平均$100超、Q3 $120・Q4 $115 | Brent $92.56は予想を下回る |

| EIA | Brent | 戦争で従来予測比$20高 | 下方 |

| LiteFinance | Brent | $100〜$125レンジ | 下方 |

| J.P. Morgan | Brent | 2026年平均$60前後 | 5月末はこれを上回る |

4月時点では「ホルムズ海峡閉鎖長期化」を前提とした強気(高値)予想が中心でしたが、5月の終戦交渉進展と原油価格の下落により、足元の水準はJ.P. Morganを除く各社の想定を下回っています。

April forecasts were dominated by bullish projections based on extended Hormuz closure. May’s peace progress and price decline have moved current levels below most institutional forecasts, with J.P. Morgan as the exception.

3-3. 価格下落の背景 / Drivers of Price Decline

サウジとUAEは一部の輸出を海峡外で積み込むターミナルへ転送することに成功。消費国の商業・政府戦略備蓄も市場に放出され、3〜4月で世界の石油在庫は2.5億バレル(日量400万バレル)取り崩されました。

Saudi Arabia and UAE successfully diverted some exports to terminals outside the Strait. Consumer commercial and government strategic reserves were released, drawing down global oil inventories by 250M barrels (4M bpd) during March-April.

大西洋岸の原油輸出は2月以降日量350万バレル増加し、主にスエズ以東の被害市場へ向かっています。米国・ブラジル・カナダ・カザフスタン・ベネズエラから顕著な増加。ロシアの原油輸出も、製油所への度重なる攻撃で精製能力が削減された結果、増加していると報じられています。

Atlantic Basin crude exports rose 3.5M bpd since February, mainly directed to affected markets east of Suez. Notable increases from US, Brazil, Canada, Kazakhstan, and Venezuela. Russian crude exports also reportedly increased due to refinery capacity reductions from repeated strikes.

ゴールドマンの分析では、価格高騰と供給不足による相当な需要破壊が起きているため、市場が想定より「やや低い水準」で再均衡しているとされます。需要喪失はアジアの航空・石油化学セクターで既に非常に大きいと指摘されています。

Goldman Sachs analysis suggests substantial demand destruction from price spikes and supply shortages, with the market rebalancing ‘somewhat lower’ than expected. Demand losses in Asian aviation and petrochemical sectors are already significant.

3-4. 今後の見通し / Outlook

IMC国際資本市場協会のシニアアドバイザーBob Parkerは、原油価格は「今後少なくとも数ヶ月は」$90-100の間で推移する見込み、永続的和平合意のより明確な見通しが立つまでと発言。「仮にホルムズ海峡が開いても、その開放は部分的なものになると言うのが公平だ」と述べています。

Bob Parker, Senior Adviser at IMC, expects prices to trade in the $90-100 range ‘for at least several months’ until clearer prospects for a permanent peace deal emerge. ‘It is fair to say that even if Hormuz opens, that opening will be partial.’

EIAは戦略予測でホルムズ海峡が5月末まで実質閉鎖、6月から徐々に回復、年後半に戦前水準に戻ると想定。湾岸6か国(イラク・サウジ・クウェート・UAE・カタール・バーレーン)から日量約1,050万バレルが戦闘期間中に集合的に停止。戦前の生産・貿易パターンに戻るのは2026年末〜2027年初と見込まれています。

EIA’s strategic forecast assumes Hormuz remains effectively closed until end-May, gradually recovering from June, and returning to pre-war levels in late 2026. The six Gulf states collectively shut in approximately 10.5M bpd during the conflict period. Return to pre-war production and trade patterns expected by late 2026 / early 2027.

3-5. UAE OPEC脱退後の動向 / UAE Post-OPEC Withdrawal

UAEは5月1日付でOPEC脱退が発効しました。詳細はIssue 4で整理しており、5月時点での主要動向は以下の通りです。

UAE’s OPEC withdrawal took effect May 1. Detailed background was covered in Issue 4. Key May developments below.

- ホルムズ封鎖により湾岸産油国に経済的分断が生じており、サウジ・オマーンは紅海ルートで原油の大部分を輸出可能で「windfall(棚ぼた)」、UAEは石油収入が急減

Hormuz closure created economic divergence among Gulf producers. Saudi and Oman benefited from Red Sea route ‘windfalls,’ while UAE oil revenues plummeted. - Goldman Sachsの分析では、価格上昇分でサウジは輸送損失を補って余りあるが、UAEは部分的にしか緩和できない

Goldman Sachs analysis: Saudi price gains more than offset transit losses, but UAE only partially mitigated. - UAEのガソリン価格、5月Super 98はDh3.66/L(4月Dh3.39から上昇)、Special 95はDh3.55(前月Dh3.28)

UAE gasoline prices in May: Super 98 at Dh3.66/L (up from Dh3.39 in April), Special 95 at Dh3.55 (up from Dh3.28).

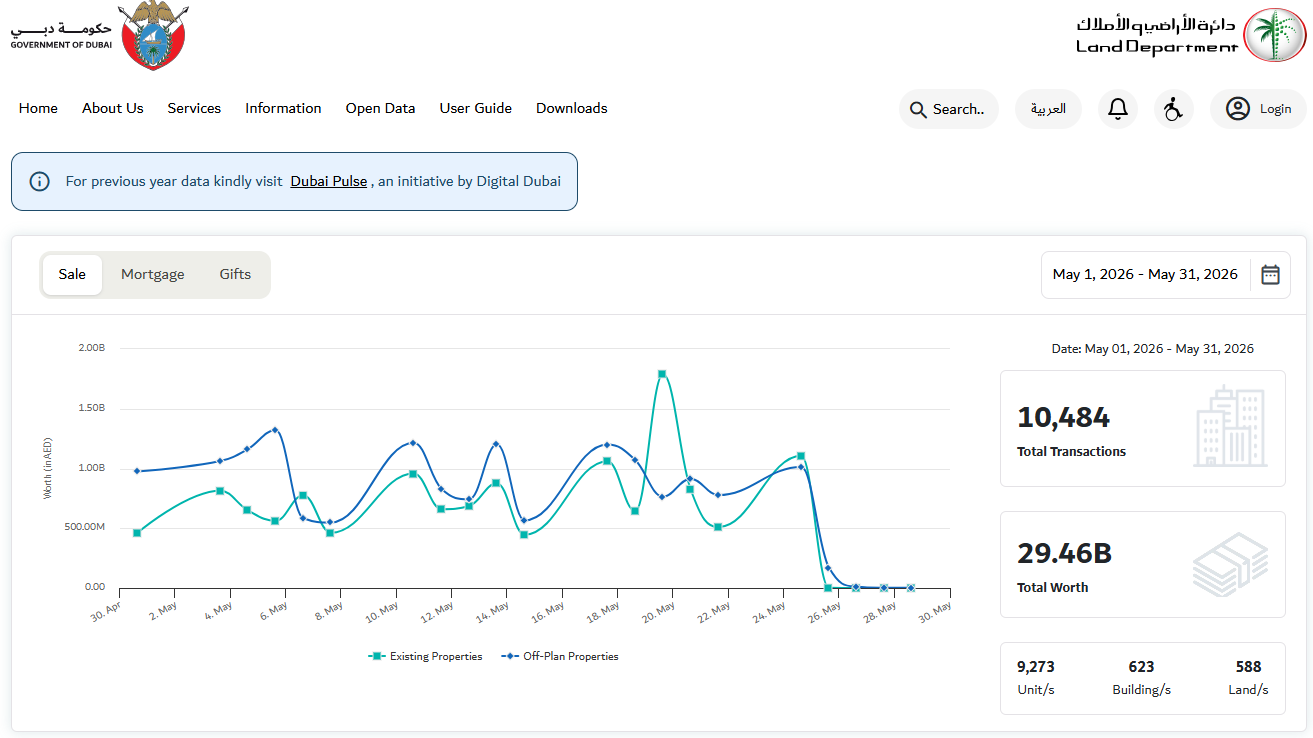

4. ドバイ不動産市場 / Dubai Real Estate Market

4-1. DLD公式データ:2月〜5月の推移 / DLD Official Data: February-May Trend

| 項目 / Item | 2月(戦前) | 3月 | 4月 | 5月 |

|---|---|---|---|---|

| 取引件数 | 17,010 | 13,242 | 14,083 | 10,483 |

| 取引額 | AED 60.72B | AED 42.61B | AED 48.43B | AED 29.46B |

| 1件平均 | AED 3.57M | AED 3.22M | AED 3.44M | AED 2.81M |

Source: Dubai Land Department (dubailand.gov.ae)

5月のデータには、月末のEid al-Adha連休(5/26〜31)による登記事務停止の影響が含まれています。営業日ベースで見ると、5月の実勢は3月・4月との中間水準で推移したと見られます。

May data includes the impact of end-month Eid al-Adha holidays (May 26-31) when registration offices were closed. On a business-day basis, May’s underlying activity appears to fall between March and April levels.

5月20日には取引額に顕著なスパイクが見られますが、同日の生データを確認すると複数の大型案件が集中しています。特にTrade Center First の商業用土地1件がAED 11億で登記されており、同日最大の取引となっています(㎡単価AED 473,611、面積2,322.58㎡)。他にPalm Jumeirah商業用土地AED 1.45億、Palm Deira住宅26件AED 1.16億、Madinat Al Mataar(Azizi Venice)住宅96件AED 8,882万等が同日に登記されています。

A notable spike on May 20 reflects multiple large transactions concentrated on that day. Notably, one Trade Center First commercial land transaction was registered at AED 1.1B (per-sqm AED 473,611, area 2,322.58 sqm) — the largest of the day. Other May 20 registrations included Palm Jumeirah commercial land AED 145M, Palm Deira residential 26 units AED 116M, and Madinat Al Mataar (Azizi Venice) residential 96 units AED 88.8M.

4-2. 登記タイムラグと解釈 / Registration Lag and Interpretation

ドバイの不動産取引は、契約から登記までに6〜12週間程度のタイムラグがあるとされています。これを踏まえると、現時点(5月末)のDLDデータが反映しているのは概ね3月の契約意欲です。

Dubai real estate transactions reportedly have a 6-12 week lag between contract and registration. Accordingly, current (end-May) DLD data primarily reflects contract activity from approximately March.

弊社は4月初旬発行のIssue 3において、3月のDLDデータが戦争開始前の契約も含む可能性を指摘し、「4月以降のデータが試金石となる」と整理しました。その後の推移を踏まえると、戦争影響の本格的な反映は4月よりも5月にずれ込んでいる可能性があります。

In Issue 3 (early April), we noted that March DLD data may include pre-war contracts and identified ‘April onwards as the litmus test.’ Subsequent developments suggest the substantive reflection of war impact may have shifted from April to May.

契約から登記までのタイムラグを考慮すると、和平交渉進展(5月)・原油価格下落・Eid連休後の活動再開といった5月以降の動きが数字に反映されるのは、7月〜9月のデータからとなる見込みです。さらに、戦時下中盤(4〜6月)の契約意欲そのものは、8〜10月のデータでより明確になります。継続監視いたします。

Given the registration lag, May’s developments (peace negotiation progress, oil price declines, post-Eid recovery) will likely appear in data from July-September. The contract activity from the mid-war period (April-June) will become clearer in August-October data.

3月と4月の数字は依然として戦前の取引を反映している。全面的な影響は第2四半期まで明らかにならない可能性が高い

— Ronan Arthur氏、Cavendish Maxwell住宅評価責任者 / Cavendish Maxwell, AGBI, May 2026

4-3. Property Finder VPI / Property Finder Value Performance Index

4月27日発表のProperty Finder(ドバイ大手不動産情報プラットフォーム)のValue Performance Index(VPI)の主要数値は以下の通りです(Issue 4既出データ、5月の追加発表は本号発行時点で未公表)。

Property Finder VPI key figures (April 27 release; data covered in Issue 4, May update not yet released as of this issue).

- VPI:229.2、月次▼5.9%(年初来は+8.9%)

VPI: 229.2, MoM ▼5.9% (YTD +8.9%). - アパートメント:月次▼6.3%、ヴィラ:月次▼5.8%

Apartments: MoM ▼6.3%; Villas: MoM ▼5.8%. - 主要下落エリア:Arabian Ranches Phase 2 ▼11.5%、Dubai Hills Estate ▼10.8%、JVC ▼10.3%、Burj Khalifaアパート▼10.2%、Palm Jumeirah ▼8.4%

Major decline areas: Arabian Ranches Phase 2 ▼11.5%, Dubai Hills Estate ▼10.8%, JVC ▼10.3%, Burj Khalifa apartments ▼10.2%, Palm Jumeirah ▼8.4%. - 賃料動向(1〜2月比):UAE全体▼5.4%、ドバイ▼6.7%、Downtown・Palm・JLT等プライムエリアは最大▼15%

Rental trends (vs Jan-Feb): UAE-wide ▼5.4%, Dubai ▼6.7%, prime areas (Downtown, Palm, JLT) up to ▼15%.

4-4. 取引価格の動き / Transaction Price Trends

機会主義的な投資家が引き続き活発で、動機のある売り手からの魅力的なディールを活かしている

— Ronan Arthur氏、Cavendish Maxwell住宅評価責任者 / AGBI, May 2026

不動産仲介業者のWhatsAppグループで出回っている苦境売り(distress listing)は、10〜50%のディスカウントを示している。2026年第4四半期の引き渡し前に『元の価格を下回る緊急売却』を打ち出す広告がある

— AGBI, May 2026

Emaar Properties創業者Mohamed Alabbar氏はBloomberg TVで、顧客の支払い延期希望について以下のように発言しています。

Emaar Properties Founder Mohamed Alabbar commented on payment deferral requests on Bloomberg TV.

40,000人の顧客がいる。12月には800〜850人が延期を求めていた。戦時中には1,050人に増えた。今は720〜750人

— Mohamed Alabbar氏、Emaar Properties創業者 / Bloomberg TV

4-5. Emaar Properties(ドバイ政府系デベロッパー) Q1 2026決算 / Emaar Q1 2026 Earnings

- 税引後純利益:AED 64億(前年比+38%) *約2780億円

Net profit after tax: AED 6.4B (+38% YoY). - 収益:AED 124億(前年比+23%) *約5400億円

Revenue: AED 12.4B (+23% YoY). - 不動産販売額:AED 224億(前年比+16%) *約9700億円

Property sales: AED 22.4B (+16% YoY). - 収益バックログ:AED 1,634億(前年比+29%) *約7兆円

Revenue backlog: AED 163.4B (+29% YoY).

不動産デベロッパーの会計上の特性として、「不動産では、Sales(販売)≠Revenues(収益)」とされており、収益(Revenue)は工事進捗に応じた繰延計上、バックログは契約済みで未計上の販売を含みます。第1四半期(1〜3月)のうち戦争期間は3月1ヶ月のみで、約9700億円の不動産販売が記録されています。また前年同期(2025年Q1)も記録的な水準であったとされています。

In real estate developer accounting, ‘Sales ≠ Revenues’ — Revenue is deferred recognition based on construction progress, and backlog includes contracted but unrecognized sales. Only March of Q1 (Jan-Mar) was within the war period, and Q1 2025 was also reportedly a record level.

5. ホスピタリティ・観光・F&B / Hospitality, Tourism & F&B

5-1. ホテル稼働率と閉鎖状況 / Hotel Occupancy & Closures

ホスピタリティ全体にとってハルマゲドン・シナリオ。2026年は観光フローがパンデミック的に止まるのとほぼ同じ

— Elena Stock氏、Fitch Ratingsディレクター / Fitch Ratings

Moody’sはホテル稼働率の見通しについて、2月の80%から第2四半期に10%まで低下する見込み、ホスピタリティセクターの大部分の事実上の停止に相当するとの分析を示しています。

Moody’s projects hotel occupancy to fall from 80% in February to 10% in Q2 — equivalent to a de facto shutdown of much of the hospitality sector.

UAE全体の消費影響について、「UAE総消費は今年、従来予想比で約12%減少しうる。ただしその減少の約70%は住民ではなく観光客から来る」(Redseer Strategy Consultantsアナリスト)との分析が示されています。

On UAE total consumption: ‘Total UAE consumption could decline by about 12% versus prior expectations. About 70% of that decline comes from tourists rather than residents’ (Redseer Strategy Consultants).

5-2. F&Bセクターの動向 / F&B Sector Dynamics

AGBIは4月時点で、ドバイのレストランが夏までの閉鎖可能性を警告していると伝えています。Tourism Economics(Oxford Economicsの一部門)はレストラン業界が観光客減により給与30%削減等の影響を受けていると分析しています。

AGBI reported in April that Dubai restaurants were warning of closure possibilities by summer. Tourism Economics analyzed that the restaurant industry has been impacted with salary cuts of around 30% due to tourist decline.

自己資金で運営する多くのレストランには、キャッシュフローなしで6ヶ月持ちこたえる余裕はない

— Panchali Mahendra氏、Atelier House Hospitality CEO / AGBI, April 2026

2023年に1,715万人の国際宿泊客を受け入れていたドバイ観光セクターは、戦争開始後70〜80%の収入減少に直面。Tourism Economicsの推計では、2,300万〜3,800万人の旅行者が減少する可能性と報じられています。

Dubai’s tourism sector, which received 17.15M international overnight visitors in 2023, faces 70-80% revenue decline since war began. Tourism Economics estimates indicate 23-38M potential traveler decline.

複数の業界報道が、戦争開始後のF&B業界における運転資金圧迫や売却動機の増加について伝えています。Downtown・Marina等の観光客比率が高いエリアにおいて、戦前比で半減水準まで売上が落ち込むケースが業界関係者から報告されているとされています。

Multiple industry reports describe working capital pressure and increased sales motivation in F&B since war began. Areas with high tourist exposure (Downtown, Marina) reportedly experiencing sales declines to about half of pre-war levels per industry sources.

戦争開始当初は、F&B事業者の多くが「市場は戻ってくる」との見方を維持していたと報じられています。一方、5月時点では運転資金の枯渇や賃貸借契約の更新期到来等を背景に、より柔軟な価格交渉に応じる事業者も出始めているとされています。

At war’s outset, many F&B operators reportedly maintained the view that ‘the market will return.’ By May, however, with working capital depletion and lease renewal timing, more operators are reportedly engaging in flexible price negotiations.

市場が不確実な時、売り手にとって最悪なのは、決して来ないかもしれない買い手を待ちながら、過大評価された掲載に何ヶ月も座り続けることだ

— Jack Sellers氏、YallaValue創業者 / AGBI, May 2026

5-3. 倒産・救済策の動向 (ドバイ市場) / Insolvency Dynamics and Government Measures (Dubai Market)

ドバイ市場における倒産関連の動向は、足元では政府・中央銀行による救済措置の影響を受けています。これらの措置によって、表面化する倒産件数は抑制されている一方、不良債権予備軍が増加している可能性が指摘されています。なお、本セクションで言及している救済措置と倒産動向はドバイ市場の状況に基づくものであり、UAE全体・他首長国・近隣諸国における状況とは異なる場合があります。

Dubai market insolvency dynamics are currently influenced by government and central bank relief measures. These measures suppress the surfacing of insolvency cases, while pointing to potential growth in non-performing loan reserves. The relief measures and insolvency trends discussed in this section apply specifically to the Dubai market and may differ from conditions in the broader UAE, other Emirates, or neighboring countries.

- UAE中央銀行(3月17日):紛争関連の影響ローンを高リスクカテゴリに即時移行することを回避する一時的柔軟性を導入(5本柱金融機関レジリエンス・パッケージ)

UAE Central Bank (March 17): Temporary flexibility introduced to avoid immediate migration of conflict-affected loans to higher-risk categories (Five-Pillar Financial Institution Resilience Package). - 緊急ビジネス基金 AED 50億(2026年3月導入)

Emergency Business Fund AED 5B (introduced March 2026). - 商業賃料90日凍結(自動・申請不要、2026年3月)

Commercial rent freeze for 90 days (automatic, no application required, March 2026). - ドバイ当局のビジネス支援パッケージ AED 10億(4月1日発効)

Dubai authorities’ business support package AED 1B (effective April 1). - 5月21日、ドバイは追加のAED 15億の経済刺激パッケージを承認。ホテル夜間税(高級ホテルでDh20)の停止、ホテル・レストラン勘定への7%地方税の停止を含む33のイニシアチブ

May 21: Dubai approved an additional AED 1.5B economic stimulus package — 33 initiatives including suspension of hotel night tax (Dh20 at luxury hotels) and suspension of 7% municipal tax on hotel and restaurant bills. - DEWA(電気水道)支払い猶予

DEWA (electricity and water) payment grace periods.

これらの措置は、本来であれば資金繰り上の困難から倒産に至る事業者の延命に寄与する一方、措置期限切れのタイミングで「先送りされた負担」が顕在化する可能性があります。賃料凍結90日は既に5月後半に期限を迎え始めており、6〜7月にかけて段階的に措置の効果が薄れていく見込みです。

These measures support the survival of businesses that would otherwise face cash-flow-driven bankruptcy, while creating the possibility that ‘deferred burdens’ surface upon expiry. The 90-day rent freeze has already begun expiring in late May, with measures expected to lose effect gradually through June-July.

5-4. 大手機関オフィスの動向 / Major Office Movements

5月時点で、ドバイ拠点を恒久的に閉鎖した多国籍大手企業の報道は確認されていません。3月以降に報じられたオフィス退避(Goldman Sachs、Morgan Stanley、Citi、Deloitte、PwC等)はいずれも一時的(temporary)な性格のものとされています。

As of May, no reports of permanent Dubai office closures by multinationals were identified. Office evacuations reported since March (Goldman Sachs, Morgan Stanley, Citi, Deloitte, PwC, etc.) have all been characterized as temporary.

実際の影響として「リクルーターと移転コンサルタントは、外国人専門職が家族を一時的に海外移転させたり、地域への移転を遅らせたりする着実な増加を報告。多国籍企業は一部従業員を静かに欧州やアジアに移した。Dubai MarinaやDowntownの一部で、ブローカーは外国人テナントからの賃貸照会が顕著に弱まったと言う」との報道があります。

Recruiters and relocation consultants report steady increases in expat professionals temporarily moving families overseas or delaying relocations to the region. Multinationals quietly moved some employees to Europe or Asia. Brokers in Dubai Marina and Downtown report notably weaker rental inquiries from foreign tenants.

5-5. 航空動向 / Aviation

5月末のEid al-Adha連休期間中、ドバイ国際空港は域内旅行需要を取り込んでいます。Dubai空港は5月31日をEid旅行のピーク日と予想(194,500人)。国際長距離便の戦時下での減少傾向と並行して、湾岸域内の旅行需要は連休期に一定の回復を見せています。

During end-May Eid al-Adha holidays, Dubai International Airport captured regional travel demand. Dubai expected May 31 as Eid travel peak day (194,500 passengers). Alongside continued international long-haul decline, Gulf regional travel demand showed a degree of recovery during the holiday period.

6. 不動産デベロッパー債券市場 / Real Estate Developer Sukuk Market

6-1. DIB Sukuk Indicative Prices(5月22日時点) / DIB Sukuk Indicative Prices (May 22)

Dubai Islamic Bank(DIB)が公表する週次のSukuk Indicative Prices(2026年5月22日付)に基づき、ドバイおよびGCCの主要不動産デベロッパー関連Sukuk銘柄の利回り水準を整理します。当Sukukは各デベロッパーの不動産開発資金社債のような位置づけです。

Based on the weekly Sukuk Indicative Prices published by Dubai Islamic Bank (DIB) (May 22, 2026), key yield levels for Dubai and GCC major real estate developer sukuk are summarized below.

| 銘柄 / Issuer | 満期 | Coupon | DIB Buy | DIB Sell | 格付け |

|---|---|---|---|---|---|

| Emaar Properties | Sep 2029 | 3.875% | 5.58% | 4.32% | Baa1/BBB+ |

| Emaar Properties | Jul 2031 | 3.700% | 5.37% | 4.75% | Baa1/BBB+ |

| Aldar Inv. Properties | Oct 2029 | 3.875% | 5.16% | 4.67% | Baa1 |

| Aldar Inv. Properties | May 2034 | 5.500% | 5.70% | 5.42% | Baa1 |

| DP World | Sep 2030 | 3.750% | 5.72% | 5.25% | Baa2/BBB+ |

| 銘柄 / Issuer | 満期 | Coupon | DIB Buy | DIB Sell | 格付け |

|---|---|---|---|---|---|

| DAMAC Holdings | Apr 2027 | 8.375% | 8.06% | 5.41% | Ba1/BB+ |

| DAMAC Holdings | Aug 2029 | 6.125% | 7.65% | 6.74% | Ba1 |

| Sobha Realty | Jul 2028 | 8.750% | 9.39% | 8.35% | Ba2/BB |

| Sobha Realty | Sep 2030 | 7.125% | 9.31% | 8.75% | Ba2/BB |

| Omniyat | May 2028 | 8.750% | 9.96% | 8.58% | BB- |

| Omniyat | Mar 2029 | 7.250% | 10.01% | 8.83% | BB- |

| Binghatti Holdings | Feb 2027 | 9.625% | 11.71% | 9.06% | BB- |

| Binghatti Holdings | Jul 2029 | 7.750% | 11.79% | 10.85% | BB- |

| Binghatti Holdings | Aug 2031 | 8.375% | 11.42% | 10.66% | BB- |

Source: Dubai Islamic Bank — Indicative Sukuk Price as on 22-May-2026

6-2. Issue 4(4月28日時点)からの変化 / Change from Issue 4 (April 28)

- Binghatti(各銘柄レンジ):

4月28日 10.37〜11.25% → 5月22日 11.42〜11.79%(上方シフト)

Binghatti range: April 28 10.37-11.25% → May 22 11.42-11.79% (upward shift). - Sobha Realty(各銘柄レンジ):

4月28日 8.0〜8.7% → 5月22日 9.31〜9.39%(上方シフト)

Sobha Realty range: April 28 8.0-8.7% → May 22 9.31-9.39% (upward shift). - Omniyat:5月22日 9.96〜10.01%

Omniyat: May 22 9.96-10.01%. - Emaar Properties: 5月22日 5.37〜5.58%(投資適格水準を維持)

Emaar Properties: May 22 5.37-5.58% (maintained investment-grade levels). - Aldar Investment Properties: 5月22日 5.16〜5.70%(投資適格水準を維持)

Aldar Investment Properties: May 22 5.16-5.70% (maintained investment-grade levels).

投機的格付け銘柄については、和平交渉進展による全般的なリスクオン傾向が見られる中でも、利回り水準はむしろ4月末から上方にシフトする動きが確認されています。特にBinghattiの満期長め(2029年〜2031年)の銘柄については、DIB Buy利回りで11%台が継続しています。

Despite general risk-on sentiment from peace negotiation progress, speculative-grade names show yields shifting upward from end-April. Binghatti’s longer-dated (2029-2031) issues continue to print DIB Buy yields above 11%.

なお、投機的格付け組の発行時クーポン(いずれも戦前発行)は7%台前半〜8%台前半でした(Sobha Sep 2030 7.125%、Arada Aug 2030 7.15%、Omniyat Mar 2029 7.25%、Binghatti Aug 2031 8.375%)。同一銘柄の5月22日DIB Buy利回りはSobha Sep 2030が9.31%、Binghatti Aug 2031が11.42%等となっており、発行時クーポン対比で概ね+2〜3ポイントの上方シフトとなっています(Sobha Sep 2030 約+2.2pt、Binghatti Aug 2031 約+3.0pt)。

Speculative-grade issuers’ original coupons (all issued pre-war) ranged from low-7% to low-8% (Sobha Sep 2030 7.125%, Arada Aug 2030 7.15%, Omniyat Mar 2029 7.25%, Binghatti Aug 2031 8.375%). Same-issue DIB Buy yields on May 22 reached Sobha Sep 2030 9.31% and Binghatti Aug 2031 11.42%, an upward shift of roughly +2-3 points versus original coupons (Sobha Sep 2030 ~+2.2pt, Binghatti Aug 2031 ~+3.0pt).

6-3. 償還期限 / Default Status & Maturity Schedule

5月末時点で、主要デベロッパーのSukuk債務についてデフォルト(債務不履行)の公表は確認されていません。

As of end-May, no defaults on sukuk obligations of major developers have been publicly reported.

- 2026年9月:Emaar Properties AED建て分

September 2026: Emaar Properties AED issue. - 2027年2月:Dar Al Arkan、Binghatti

February 2027: Dar Al Arkan, Binghatti. - 2027年4月:DAMAC Holdings

April 2027: DAMAC Holdings. - 2027年6月:Arada Developments

June 2027: Arada Developments. - 2028年5-8月:Omniyat、DAMAC Holdings、Sobha Realty

May-August 2028: Omniyat, DAMAC Holdings, Sobha Realty. - 2029年2-7月:Sobha Realty、Binghatti、Dar Al Arkan、DAMAC Holdings、Arada Developments

February-July 2029: Sobha Realty, Binghatti, Dar Al Arkan, DAMAC Holdings, Arada Developments. - 2030年7-8月:Dar Al Arkan、Binghatti、Arada Developments

July-August 2030: Dar Al Arkan, Binghatti, Arada Developments.

6-4. 引受幹事の動向 / Lead Manager Activity

ドバイ・GCCの不動産デベロッパーが発行するSukukの引受幹事は、UAE地場銀行(Emirates NBD Capital、Abu Dhabi Commercial Bank、Dubai Islamic Bank、Abu Dhabi Islamic Bank、Mashreq、First Abu Dhabi Bank等)が中核を担い、これに国際金融機関が参加する構成が標準的となっています。2025年から2026年前半にかけての主な案件例は以下の通りです。

Sukuk bookrunners for Dubai and GCC real estate developers are typically led by local UAE banks (Emirates NBD Capital, ADCB, DIB, ADIB, Mashreq, FAB), with international banks participating. Major deals from 2025 to early 2026 are illustrated below.

Omniyat $600M Sukuk(2026年2月発行)

Joint Global Coordinators: Abu Dhabi Commercial Bank、Citi、Dubai Islamic Bank、Emirates NBD Capital、First Abu Dhabi Bank、JP Morgan、Mashreq、Standard Chartered Bank

Joint Global Coordinators: ADCB, Citi, DIB, Emirates NBD Capital, FAB, JP Morgan, Mashreq, Standard Chartered Bank.

Sobha Realty $750M Green Sukuk(2025年9月発行)

Joint Global Coordinators: Dubai Islamic Bank、Emirates NBD Capital、J.P. Morgan、Mashreq、Standard Chartered

Joint Global Coordinators: DIB, Emirates NBD Capital, J.P. Morgan, Mashreq, Standard Chartered.

Binghatti Holdings $500M Sukuk(2025年7月発行)

Joint Global Coordinators: Emirates NBD Capital、Abu Dhabi Islamic Bank、Dubai Islamic Bank、Mashreqbank

Joint Global Coordinators: Emirates NBD Capital, ADIB, DIB, Mashreqbank.

これらの案件構成から、米系(Citi、JP Morgan)・英系(Standard Chartered)・地場銀行が並立する形で参画する案件と、地場銀行が中心となり国際金融機関の関与が限定的な案件の双方が見られます。HSBC等の英系大手が単独で主導するパターンは、足元の案件では確認されていません。

These compositions show two patterns: deals with US (Citi, JP Morgan), UK (Standard Chartered), and local banks participating side-by-side; and deals centered on local banks with limited international participation. Patterns of HSBC or similar UK majors leading solo were not identified in recent transactions.

7. サウジアラビア・アブダビ不動産市場 / Saudi Arabia & Abu Dhabi Real Estate

本号より、ドバイ以外のGCC主要不動産市場、特にサウジアラビアとアブダビについて独立したセクションを設けます。両市場ともドバイとは異なる市場性格・需要構造を持っており、戦争影響の出方や統計データの公開頻度にも違いがあります。両市場のデータは現時点で2026年第1四半期(1〜3月)分が中心となっており、戦争(2月28日開始)の影響は限定的にしか反映されていません。本格的な反映は第2四半期(4〜6月)データ(7〜8月発表予想)以降と見込まれます。

From this issue, we introduce a dedicated section for major GCC real estate markets outside Dubai — Saudi Arabia and Abu Dhabi. These markets have different market characters, demand structures, and statistical disclosure cadence than Dubai. Current data centers on Q1 2026 (Jan-Mar), with limited war impact (February 28 start) reflected. Substantive reflection expected from Q2 data (July-August release) onwards.

7-1. アブダビ不動産:Q1 2026 Abu Dhabi Real Estate Q1 2026

- 取引総額:AED 660億(前年同期AED 253億から約+161%)

Total transaction value: AED 66B (vs AED 25.3B prior-year quarter, ~+161%). - 取引件数:13,518件(前年同期6,896件から約+96%)

Transaction count: 13,518 (vs 6,896 prior-year quarter, ~+96%). - うち売買取引額:AED 510億(+228.6%)、売買取引件数:8,940(+134%)

Of which sale-purchase: AED 51B (+228.6%) / 8,940 transactions (+134%). - 主要エリア:Hudayriyat Island(AED 119.7億)、Reem Island(AED 94.5億)、Saadiyat Island(AED 88億)。いずれも政府主導のmaster-planned developmentが立地するエリア

Top areas: Hudayriyat Island (AED 11.97B), Reem Island (AED 9.45B), Saadiyat Island (AED 8.8B) — all government-led master-planned development zones. - Repeat lease price index は 2025 年 3 月比で+16%上昇

Repeat lease price index +16% vs March 2025.

Q1 2026 は 1 月・2 月が戦前、3 月のみ戦争期間にあたります。さらに不動産取引には契約から登記までのタイムラグがあるため、当四半期のデータは戦前から積み上がってきた契約の登記を多く含むと見られます。戦争影響の本格的な反映は、Q2(4〜6 月)データ(7月発表予想)以降と見込まれます。

Q1 2026 covers January-February (pre-war) and only March (in-war). Given the contract-to-registration lag, Q1 data likely contains many registrations of pre-war contracts. Substantive war impact reflection expected from Q2 (April-June) data, with anticipated release in July.

7-2. サウジアラビア不動産:Q1 2026 Saudi Arabia Real Estate Q1 2026

- 全国 Q1 2026 取引額:SAR 1,120億(約298.5億ドル、前年比+6.8%)

National Q1 2026 transactions: SAR 112B (~$29.85B, +6.8% YoY). - リヤド住宅(Q3 2025):13,000件、SAR 176億(約46.9億ドル、前四半期比+18.7%、前年同期比▼44.3%)

Riyadh residential (Q3 2025): 13,000 transactions, SAR 17.6B (~$4.69B, +18.7% QoQ, -44.3% YoY). - ジェッダ(Q3 2025):7,500件、SAR 87億(約23.1億ドル、前四半期比+10.3%、前年同期比▼19.3%)

Jeddah (Q3 2025): 7,500 transactions, SAR 8.7B (~$2.31B, +10.3% QoQ, -19.3% YoY). - ダンマン(Q3 2025):3,000件、SAR 32億(約8.5億ドル、前年同期比+60%、前四半期比+37%)

Dammam (Q3 2025): 3,000 transactions, SAR 3.2B (~$850M, +60% YoY, +37% QoQ). - リヤド住宅賃料:CBRE 分析では 2026 年 3 月に前年比▼2.1%軟化、JLL の年間ベースではアパート+19.6%・ヴィラ+17.2%。差異は測定時点と手法に起因

Riyadh residential rents: CBRE shows -2.1% YoY softening in March 2026; JLL annual basis shows apartments +19.6% / villas +17.2%. Differences attributed to measurement timing and methodology. - リヤド 5 年間家賃凍結が新たに導入。短期的に賃料を固定し占有者コストの上昇圧力を抑える効果(JLL)

New 5-year rent freeze in Riyadh: short-term rent stabilization expected to suppress occupier cost pressure (JLL). - サウジ平均グロス賃料利回り Q1 2026 で 6.84%。リヤド 8.89%、ジェッダ約 7.89%(STC 不動産指数)

Saudi average gross rental yield Q1 2026: 6.84%. Riyadh 8.89%, Jeddah ~7.89% (STC Real Estate Index).

7-3. サウジアラビアの不動産関連法制度 Saudi Real Estate Regulatory Reforms

2000年の旧法を置き換える新法が、2026年1月21日に施行されました。これまでの裁量的・個別許可制から、指定地域に紐づく透明で構造化されたアプローチへの転換とされ、外国人個人・外国所有法人が、施行規則に定める条件の下、正式に不動産を所有可能となりました。

The new law replacing the 2000 framework took effect January 21, 2026. The shift moves from a discretionary, case-by-case approval system to a transparent, structured approach tied to designated zones. Foreign individuals and foreign-owned entities may now formally own real estate under conditions set by implementing regulations.

【取得可能エリアの制限】 Designated Zones and Restrictions

- 外国人居住者は住宅1戸の所有が可能。非居住者は当局が承認した指定地域でのみ所有可能

Foreign residents may own one residential unit; non-residents may own only in officially approved designated zones. - 住宅所有は4都市(メッカ・メディナ・ジェッダ・リヤド)を除く全国で認められる。メッカ・メディナでの所有はムスリムに限定される

Residential ownership permitted nationwide except in four cities (Makkah, Madinah, Jeddah, Riyadh). Ownership in Makkah/Madinah restricted to Muslims. - メッカ・メディナ地域でも承認されたホスピタリティ・観光・開発プロジェクトへの外国人参加の道は確保

In Makkah/Madinah, pathways for foreign participation in approved hospitality, tourism, and development projects remain available.

【コスト・手数料 売却時に課税】

Costs and Fees — Levied at Disposal (Not Acquisition)

新法は、外国人による不動産処分(disposal=売却・譲渡)時に REGA(Real Estate General Authority)が徴収する手数料を定めています。この手数料は不動産取得時ではなく、外国人が売却・譲渡する時に課されます。

The new law defines fees levied by REGA at the time of disposal (sale or transfer) by foreigners. These fees apply at disposal, not at acquisition.

- 既存のRETT(不動産譲渡税):5%(サウジ国民・外国人を問わずすべての不動産取引に適用される既存の税)

Existing RETT (Real Estate Transfer Tax): 5% — applies to all real estate transactions regardless of nationality. - 外国人処分手数料(新設):法定上限は処分価値の最大5%

Foreign disposal fee (new): statutory ceiling at maximum 5% of disposal value.

外国人投資家が売却時に支払う合計コストは、既存のRETT 5%に加えて外国人処分手数料を上乗せする構造となり、最大で約10%となります。

Total disposal cost for foreign investors is structured as existing RETT 5% plus the new foreign disposal fee, totaling up to approximately 10%.

【実施規則の草案(2025 年公開、最終版は今後発行予定)】 Draft Implementing Regulations

- 住宅物件:2.5% Residential property: 2.5%.

- 農業・商業・工業用物件:原則0%(ただし経済都市・特別経済特区内では2.5%)

Agricultural, commercial, industrial property: 0% in principle (2.5% within economic cities or special economic zones).

この草案が最終確定すれば、外国人投資家が住宅を売却する際の実効コストは「RETT 5% + 処分手数料 2.5% = 7.5%」となる見込みです。

If finalized as drafted, the effective cost when foreign investors sell residential property would be RETT 5% + disposal fee 2.5% = 7.5%.

【罰則および取得時の費用】 Penalties and Acquisition-Time Costs

違反は最大1,000万サウジリヤルの罰金、または当該不動産価値の5%相当のいずれか高い方。虚偽情報で取得した物件は公開オークションにかけられる可能性。

新法は外国人取得時に新たな10%課税を導入するものではなく、上記の手数料はすべて売却・譲渡時に発生します。買主側の取得コストは、既存の通常手続費用(登記費用等)に従います。

Violations result in fines up to SAR 10M or 5% of the relevant property value, whichever is higher. Property acquired with false information may be subject to public auction. The new law does not introduce a 10% acquisition-time tax; all the above fees occur at disposal. Buyer-side acquisition costs follow existing ordinary procedural costs.

2025 年 11 月に REGA が国内初の公式トークン化不動産取引を完了(NHC=国家住宅会社と投資家グループ間、政府規制監督下では世界初)。2026 年 1 月にトークン化技術標準を公表し、サウジは国家不動産登記簿に直接トークンを紐づけた世界初の国の一つとなった。2026 年 2月、REGA は規制サンドボックスで 9 社のテック企業にライセンスを付与。

In November 2025, REGA completed Saudi’s first official tokenized real estate transaction (between NHC and an investor group — the world’s first under government regulatory oversight). In January 2026, tokenization technical standards were published, making Saudi one of the world’s first countries to tie tokens directly to a national real estate registry. In February 2026, REGA granted regulatory sandbox licenses to 9 tech firms.

サウジは2026年6月頃に正式な不動産トークン化規則を発行する予定とされています。規制の二層構造として、REGA が不動産側を監督(原資産が適切に登記され国家システムに紐づくことを担保)、資本市場庁 CMA が投資側を監督(トークンが利益・利回り・所有権エクスポージャーを提供する場合は証券規制の対象)。

Saudi is expected to issue formal tokenization rules around June 2026. The regulatory structure is two-tiered: REGA oversees the real estate side, while the Capital Market Authority (CMA) oversees the investment side.

外国人投資家は REGA 指定ゾーンでのみトークン化された小口持分を所有可能。リヤド・ジェッダ・主要ギガプロジェクト回廊が主たる対象エリアになる見込み。本号発行時点では 6 月の正式規則は未公表であり、6 月の制度内容と運用開始時期は今後の注目事項となります。

Foreign investors will be able to hold tokenized fractional interests only in REGA-designated zones. Riyadh, Jeddah, and major gigaproject corridors are expected to be primary target areas. As of this publication, June’s formal rules have not been published; the regulatory content and start timing are key items to watch.

7-4. ハッジ2026 Hajj 2026

ハッジ(Hajj)とは、サウジアラビアの聖地メッカへ向かうイスラム教の大巡礼のことです。世界中から数百万人ものムスリム(イスラム教徒)が集まる世界最大規模の宗教儀礼で、経済的・体力的に余裕のあるすべての信者が一生に一度は行うべき「五行(宗教上の義務)」の一つとされています。

例年、多数のイスラム教徒がメッカに赴いていましたが、今年は中東地域の緊張下での動向が注目されていました。結果として、昨年より多くのイスラム教徒がメッカへ集結する状況となり、その約90%はサウジ以外の海外から終結しました。

- 総巡礼者数:1,707,301人 (2025年1,673,230人比+34,071人、2024年1,833,164人比▼125,863人)

Total pilgrims: 1,707,301 (+34,071 vs 2025’s 1,673,230; -125,863 vs 2024’s 1,833,164). - 海外からの巡礼者:1,546,655人(2025年1,506,576人から増加)

International pilgrims: 1,546,655 (up from 1,506,576 in 2025). - 国内(市民・居住者):160,646人(2025年166,654人から減少)

Domestic (citizens/residents): 160,646 (down from 166,654 in 2025). - 海外巡礼者の到着経路:航空1,485,729人、陸路54,429人、海路6,497人

International arrivals: 1,485,729 by air, 54,429 by land, 6,497 by sea.

戦争(2月28日開始)による中東地域の緊張下にもかかわらず、ハッジ2026の総巡礼者数は前年比で約34,000人増加し、海外からの巡礼者数も増加しています。儀式期間中の信者の移動は秩序立って行われたと報じられています。

Despite regional tensions from the war (started February 28), Hajj 2026 total pilgrims increased by approximately 34,000 versus prior year, with international pilgrims also rising. Movements of pilgrims during ritual periods were reported as orderly.

7-5. ドバイ・アブダビ・サウジ:データ性格の違い Data Characteristics Comparison

3市場のデータには、公開頻度・粒度に大きな違いがあります。本セクションを読む上での留意事項として整理します。

Data for the three markets differs significantly in disclosure frequency and granularity.

| 項目 / Item | ドバイ(DLD) | アブダビ(ADREC) | サウジ(REGA等) |

|---|---|---|---|

| 公開頻度 | 日次(リアルタイム) | 四半期 | 四半期 |

| 公開チャネル | dubailand.gov.ae | プレスリリース | REGA + 民間調査会社 |

| 案件単位の確認 | 可能 | 限定的 | 限定的 |

| Q2 反映時期 | 月次で確認可能 | 7月予想 | 8月予想 |

3市場の絶対値の単純比較は、市場規模・国土・人口・データ捕捉範囲が異なるため意味のある対比とはなりません。本レポートでは、変化率(前年比)、利回り(比率)、需要構造の質的整理に焦点を当てています。

Simple absolute-value comparisons across the three markets are not meaningful given differences in market size, geography, population, and data coverage. This report focuses on rates of change (YoY), yields (ratios), and qualitative demand structure.

8. GCC・グローバル波及 / GCC & Global Spillover

8-1. アジア諸国への影響 Impact on Asian Economies

ホルムズ海峡経由の原油・LNG輸出はその大半がアジア向けとなっており、戦争による湾岸エネルギー供給の混乱はアジア経済に直接的な影響を及ぼしています。

Most crude oil and LNG exports through the Strait of Hormuz are destined for Asia, making Gulf energy supply disruption a direct impact on Asian economies.

野村証券(Nomura)は、原油価格10%上昇に対する各国の経常収支悪化幅を以下のように整理しています。

Nomura analyzed the current account deterioration impact per 10% oil price increase by country.

- タイ:純原油輸入/GDP 4.7%、原油10%上昇でCA悪化 0.5pp

Thailand: net oil imports/GDP 4.7%, CA deterioration 0.5pp per 10% oil rise. - インド:純原油輸入/GDP 3.1%、原油10%上昇でCA悪化 0.4pp

India: net oil imports/GDP 3.1%, CA deterioration 0.4pp per 10% oil rise. - 韓国:純原油輸入/GDP 2.7%、原油10%上昇でCA悪化 0.3pp

Korea: net oil imports/GDP 2.7%, CA deterioration 0.3pp per 10% oil rise. - フィリピン:CA赤字国、拡大方向

Philippines: CA-deficit country, deterioration direction. - マレーシア:原油輸出国、プラス影響

Malaysia: oil exporter, positive impact.

- インド:米国はインドに対しロシア産原油の購入を30日間許可する許容で合意。インド国内ではレストランが閉店の可能性を警告、政府が世帯向けガス供給を優先

India: US granted 30-day waiver for Russian oil purchases. Indian restaurants warned of possible closures; government prioritized household gas supply. - タイ:公務員の海外渡航停止、政府機関内でエレベーターでなく階段を使うよう要請

Thailand: suspended overseas travel for civil servants; requested use of stairs over elevators in government offices. - フィリピン:原油の90%以上を輸入。一部政府機関で一時的な週4日勤務を導入。インフレは2026年2月に前年比+2.4%まで再上昇

Philippines: imports over 90% of oil. Temporary 4-day work week in some government offices. Inflation rose to +2.4% YoY in February 2026. - 韓国:中東から原油の70%を輸入。李在明大統領は約30年ぶりに燃料価格上限を導入、パニック買い注意を喚起

Korea: 70% of oil from Middle East. President Lee Jae-myung introduced fuel price cap for the first time in ~30 years; warned against panic buying. - ベトナム:エネルギー備蓄が20日未満と薄く、政府は在宅勤務を奨励

Vietnam: energy reserves under 20 days; government encouraged remote work.

8-2. 日本への影響 Impact on Japan

- 円ドル相場は5月にかけて1ドル=159〜160円近辺で推移、輸入物価の圧力が継続

JPY/USD traded around 159-160 yen through May; import price pressure continued. - 日銀は6月15-16日の金融政策決定会合で政策判断を予定

BOJ scheduled monetary policy meeting on June 15-16. - ガソリン価格・電力料金への上昇圧力が継続

Continued upward pressure on gasoline and electricity prices. - 中東原油の依存度は引き続き高水準であり、サウジ・UAE・カタールが主要供給国Middle East oil dependence remains high, with Saudi, UAE, and Qatar as major suppliers.

8-3. GCC全体への国際評価 International Assessment of GCC

- サウジアラビア:+3.1%(代替石油パイプライン、紅海ヤンブー経由)

Saudi Arabia: +3.1% (alternative oil pipeline via Red Sea Yanbu). - UAE:+3.1%(プラス成長維持)

UAE: +3.1% (maintained positive growth). - オマーン:+3.5%(ホルムズ外に海上出口)

Oman: +3.5% (sea outlet outside Hormuz). - カタール:縮小見込み(インフラ被害甚大)

Qatar: contraction expected (severe infrastructure damage). - バーレーン:縮小見込み(政府総債務GDP比152.4%)

Bahrain: contraction expected (government debt 152.4% of GDP). - クウェート:縮小見込み(ホルムズ依存大)

Kuwait: contraction expected (high Hormuz dependence).

- 外国人投資家のGCC株式:Q1 2026に14.7億ドル買い越し(前四半期3.1億ドル売り越しから反転)

Foreign investor GCC equity flows: Q1 2026 net buying $1.47B (reversed from prior quarter’s $310M selling). - 湾岸ソブリン債券:戦争開始以降下落、4月8日の暫定停戦発表以降は概ね反発

Gulf sovereign bonds: declined since war start; broadly recovered after April 8 interim ceasefire announcement. - サウジFDI(外国直接投資):2025年Q3前年比+34.5%増の66億ドルから、戦争影響により2025年Q4・2026年Q1にはモメンタムが停滞した可能性

Saudi FDI: from Q3 2025’s +34.5% YoY ($6.6B) to potential momentum stall in Q4 2025 / Q1 2026 due to war impact. - 食料輸入依存:UAE・カタール・バーレーン・クウェートで食料消費の80%超、サウジ・オマーンも50%超

Food import dependence: UAE, Qatar, Bahrain, Kuwait at over 80% of food consumption; Saudi and Oman over 50%. - 水資源依存:UAE・カタール・バーレーンで総水供給の40%以上を海水淡水化に依存

Water dependence: UAE, Qatar, Bahrain depend on desalination for over 40% of total water supply. - ICAEW(2026年GCC家計消費見通し):+1.4%へ2.6ポイント下方修正、2027年は+6.4%回復見込み

ICAEW (2026 GCC household consumption outlook): revised down 2.6pp to +1.4%; expected recovery to +6.4% in 2027.

8-4. 専門家・研究機関の声 Expert & Research Institution Views

【ブランド毀損論】 Brand Damage Thesis

これはドバイの究極の悪夢だ。その本質は紛争地域における安全なオアシスであることに依存していた。レジリエントになる道はあるかもしれないが、もう後戻りはできない

— Cinzia Bianco氏、欧州外交評議会(ECFR) / CNN取材

ドバイの開放性は旅行・物流・信頼へのショックに対する脆弱性を生む。一方アブダビのバランスシートとエネルギー資産が連邦に打撃吸収能力を与える

— 国際金融協会(IIF)

【ストレステスト評価】 Stress Test Perspective

一方、市場崩壊ではなく緩やかな調整と見る分析もあります。「多くの専門家はドバイ不動産市場が崩壊より緩やかな調整に向かうと見る」「特に超高級セグメント(AED 1,000万超)はレジリエントで、2026年1月だけで990件の取引を記録」(複数の不動産業界アナリスト)。

Conversely, some analysts see gradual adjustment rather than collapse. ‘Many experts view the market as moving toward gradual adjustment rather than collapse,’ and ‘Ultra-luxury segment (AED 10M+) is particularly resilient, recording 990 transactions in January 2026 alone’ (multiple real estate analysts).

【サウジ「相対的勝者」論】 Saudi as Relative Beneficiary

サウジは経済地理を再評価し、ホルムズ依存を減らして紅海へ政策を再配向している。西海岸の港湾・工業地帯・観光開発が優先事項に。二つの海岸線を持つ地理的優位は近隣国(特にUAE)に対する差別化要因

— Chatham House

ただしサウジ自体もVision 2030の見直しを進めており、戦前から国家開発計画の広範な再評価が進行していたとされる(Clingendael Instituteの分析)。

However, Saudi Arabia itself has been progressing reviews of Vision 2030, with broad reassessment of the national development plan reportedly underway pre-war (Clingendael Institute).

9. EX Group 事業状況 / EX Group Business Update

9-1. 全体方針 — AM業務への注力 Overall Direction — Focus on Asset Management

弊社は、戦争開始から3ヶ月が経過した5月時点で、引き続き各事業の継続運営とステークホルダーの皆様への情報発信を進めております。

Three months into the war, EX Group continues to operate each business line and maintain information delivery to stakeholders.

5月時点における中東情勢の推移、各市場のデータ動向、そして弊社へのお問い合わせ内容の傾向を踏まえ、今後はアセットマネジメント (AM)業務の受託への注力を一段と強める方針です。独立系AM会社として、投資家の皆様の長期的な資産保全と成長の支援に集中してまいります。

In light of evolving market conditions, data trends, and the nature of inquiries received in recent months, EX Group will further strengthen its focus on asset management (AM) business. As an independent asset management firm, we will concentrate on supporting our investors’ long-term asset preservation and growth.

【受託拡大の背景 — 増加するご相談】 Background of Expanded Mandates

- 既存物件の運用方針(売却・保有・追加投資)の判断支援

Decision support on existing property strategy (sale, hold, additional investment). - 戦争期間中の賃料・稼働率動向のモニタリング

Monitoring of rental and occupancy trends during the war period. - デベロッパー側のスケジュール・財務状況の継続的な確認

Continuous monitoring of developer schedules and financial conditions. - 戦時下・戦後の市場におけるポートフォリオ再構築の検討

Portfolio reconstruction considerations for in-war and post-war market environments.

弊社は今後、こうしたニーズに応じる形で、アセットマネジメント業務の受託を段階的に拡大してまいります。独立系AM会社として、特定デベロッパーや特定ブローカーから独立した立場で、投資家の皆様にとって最適な判断材料の提供と、長期的な視点に基づく運営支援を行います。

EX Group will progressively expand AM mandates in response to these needs. As an independent asset management firm, free from specific developers or brokers, we provide optimal decision-making material and long-term-oriented operational support to investors.

9-2. 各事業の状況 Status of Each Business Line

EXGROW Properties LLC — Real Estate Operations

- 弊社関与物件(お客様投資物件を含む)への直接被害なし

No direct damage to EXGROW-related properties (including client-invested properties). - オフプランプロジェクトの即時工事停止は確認されていない

No immediate construction stoppages confirmed for off-plan projects. - 一部投資家からのお問い合わせ増加に対し、個別にコミュニケーション実施中

Responding individually to the increased volume of investor inquiries. - 引渡しスケジュールへの変動リスクはデベロッパーおよびプロジェクトごとに異なり、変動が生じた場合は速やかに個別にご報告

Delivery schedule risks vary by developer and project; any changes will be promptly reported individually.

EXGROW Investments LLC — F&B Operations

- 現時点で店舗取得は未実施

Store acquisition is not yet been executed. - ドバイ・サウジ市場におけるカフェ・レストランの売り物件情報の収集を継続

Continuing to gather sale information on cafe and restaurant properties in Dubai and Saudi markets. - 戦争期間中の市場動向、賃料水準、立地条件、売主の価格交渉姿勢等を観察

Observing market trends, rental levels, location conditions, and seller negotiation posture during the war period. - 適切なタイミング・条件での店舗取得機会を見極め中

Evaluating opportunities for store acquisition at appropriate timing and terms.

Renewable Energy — Japan Battery Storage

- 戦争による直接的な事業影響はなし

No direct business impact from the war. - 日本側ではアセットマネジメント事業の受託や発電所の運用に注力

On the Japan side, focusing on asset management mandate expansion and power plant operations. - 開発・運用・アセットマネジメントを含むバリューチェーン全体を網羅できる体制を構築中

Building a comprehensive value chain capability spanning development, operations, and asset management. - 国内エネルギー需要・電力料金動向を継続モニタリング

Continuing to monitor domestic energy demand and electricity rate trends.

- サウジアラビアにおける食品流通事業として、現地パートナーと継続協議中

Saudi Oasis (healthcare): continuing discussions with local partners on Saudi healthcare business. - サウジ食品トレーディング(日本食品輸出・抹茶): 準備段階として継続、サウジ国内の食品流通・物流ルートの確認を継続

Saudi Food Trading (Japanese food exports — matcha): continuing preparatory stages with food distribution and logistics route verification in Saudi Arabia.

9-3. 投資家向けコミュニケーション Investor Communication

- 情勢に重大な変化が生じた場合は、本レポートの臨時版を速やかに配信

In case of significant developments, an interim edition will be distributed promptly. - 個別のご質問・ご相談は、弊社代表またはご担当者まで随時お問い合わせください

Individual questions or consultations may be addressed to the EX Group representative or your point of contact at any time. - 月次レポートは原則として各月末データ確定後約1週間日以内に発行

Monthly reports are issued within 5 days of end-of-month data confirmation as a rule.

弊社は、断定的な見通しや投資推奨を行うのではなく、公表情報・公式発表・統計データに基づく事実整理を通じて、投資家の皆様がご自身で判断される際の情報基盤を提供することを目的としています。

Rather than offering definitive forecasts or investment recommendations, EX Group aims to provide an informational foundation for investors’ independent judgment through fact-based organization of publicly disclosed data and statistics.

10. リスク評価マトリックス / Risk Assessment Matrix

EXグループとして、投資家・パートナーの皆様に対し、現時点でのリスク要因を明示する責務があると考えます。本マトリックスは公表情報・公式発表に基づくリスク項目の整理であり、確率や優先度の断定的評価は含みません。各項目について、弊社が現在どのような注視レベルで状況を追っているかを示しています。

As EX Group, we consider it our duty to clearly disclose risk factors to our investors and partners. This matrix presents risk factors based on publicly disclosed information; it does not include definitive evaluations of probability or severity. Each item indicates EX Group’s current level of attention rather than a risk-grade judgment.

| 注視レベル / Level | リスク項目 / Risk Item | 見解 / View |

|---|---|---|

| 要注意 | 和平交渉の停滞・決裂 | 5月28日に米イラン暫定MOU到達と報じられるも、29日以降のホワイトハウス追加要求で詰め交渉は停滞。ホルムズ管理権・ウラン濃縮の扱いが未解決。決裂時は再エスカレーションの可能性を含んでいます。 |

| 要注意 | レバノン情勢の継続 | イスラエル・ヒズボラ間の戦闘は米イラン交渉の枠外で継続。5月28日にベイルート3週ぶり空爆、5月30日にKiryat Shmonaへのロケット攻撃。地域全体の地政学リスクプレミアムが残存。 |

| 要注意 | ドバイ国内経済: 救済策期限切れに伴う先送り負担の顕在化 |

UAE中央銀行の不良債権分類凍結、賃料凍結90日、緊急ビジネス基金等によって、ドバイ市場における倒産件数は抑制されています。 賃料凍結90日は既に5月後半から期限を迎え始めており、6〜7月の動向が論点。 |

| 監視継続 | ドバイ不動産市場の動向 (7〜9月データ) |

5月DLDデータは件数▼38%(戦前比、Eid連休影響含む)。登記タイムラグを考慮すると現在の数字は3月契約意欲を反映。戦争影響の本格反映は7〜9月データから。 |

| 監視継続 | F&B・ホスピタリティセクターの収益動向 | Moody’sはホテル稼働率の第2四半期10%予測。Tourism Economicsは観光収入70〜80%減と分析。F&B業界では運転資金圧迫と価格交渉局面の変化が業界関係者から報告されている。 |

| 監視継続 | 投機的格付けデベロッパーSukuk(開発資金の社債)の利回り | 5月22日時点でBinghatti 11.4〜11.8%、Omniyat 9.96〜10.01%、Sobha 9.31〜9.39%等。4月末からの上方シフトが確認される。投資適格組(Emaar・Aldar)は5%台前半〜半ばで推移。 |

| 監視継続 | エネルギー価格の動向と物理的供給回復ペース | 5月末時点で3指標は概ね収斂(Brent $92.56、WTI $87.18、Dubai/Oman現物約$95-100)。和平合意の帰結と物理的供給回復ペース次第で再変動の可能性。 |

| 影響限定 | 建設スケジュール遅延 供給増のリスク |

資材調達・輸送コスト上昇のリスクは継続するが、5月時点で弊社関与プロジェクトの即時工事停止は確認されていない。 |

| 影響限定 | 直接物的被害 | 5月時点でUAE防空システムは高い迎撃率を維持。弊社関与物件への直接被害は未確認。 |

| 影響限定 | 多国籍企業のドバイ拠点恒久閉鎖 | 5月時点で多国籍企業によるドバイ拠点の恒久閉鎖の公表報道は確認されていない。一時的退避や新規進出判断の停滞は報告されている。 |

10-1. リスクの相互関係について On Interrelationships Among Risks

上記リスクは相互に関連しています。和平交渉の帰結はエネルギー価格・不動産需要・ホスピタリティ稼働率の全てに影響し、救済策期限切れタイミングはF&B・建設業界のキャッシュフローと連動します。本マトリックスは個別リスクの整理であり、全体としての複合的影響については各セクションの記述をご参照ください。

The risks above are interrelated. Peace negotiation outcomes affect energy prices, real estate demand, and hospitality occupancy. The timing of relief measure expiry is linked to F&B and construction cash flows. This matrix presents individual risks; for composite impacts, refer to each section.

11. 主要出典一覧 / Source List

本レポートは、公表情報・公式発表・各種統計データに基づいて整理しています。本号で参照した主要ソースを以下に整理します。

This report is organized based on publicly disclosed information, official announcements, and statistical data. Major sources referenced in this issue are summarized below.

■ 一次データ・公式統計 Primary Data & Official Statistics

- Dubai Land Department (DLD): https://www.dubailand.gov.ae/

- DLD Transaction Report, May 20, 2026

- Abu Dhabi Real Estate Centre (ADREC) — Q1 2026 Press Release

- General Authority for Statistics (GASTAT), Saudi Arabia — Hajj 2026 Final Statistics

- Real Estate General Authority (REGA), Capital Market Authority (CMA), Saudi Central Bank (SAMA)

- UAE Central Bank — Financial Institution Resilience Package

- U.S. Energy Information Administration (EIA)

- International Monetary Fund (IMF) — World Economic Outlook (April 2026)

- The White House Joint Readouts; Xinhua News Agency

■ 中東情勢・エネルギー Middle East & Energy

- Reuters, CNN, Bloomberg, NBC News, Fox News, CNBC, Al Jazeera

- Tasnim News Agency, The Hill, Foreign Policy, Al Mayadeen

- The Washington Post, The New York Times

- Foundation for Defense of Democracies (FDD), CSIS, International Crisis Group

- Chatham House, ECFR, Clingendael Institute

- Arab Center Washington DC, Atlantic Council, House of Commons Library

■ ホスピタリティ・不動産 Hospitality & Real Estate

- Fitch Ratings, Moody’s, S&P Global

- AGBI (Arabian Gulf Business Insight)

- Gulf News, Khaleej Times, The National

- Property Finder — Value Performance Index (VPI)

- Engel & Völkers, CBRE Middle East, JLL, Knight Frank

- Cavendish Maxwell, Colliers International

- Redseer Strategy Consultants

- Tourism Economics (Oxford Economics)

■ 債券・金融 Bonds & Finance

- Dubai Islamic Bank (DIB) — Indicative Sukuk Price as on 22-May-2026

- Khaleej Times Sukuk articles

- DDCAP — Sukuk Transaction Reports

- IFR (International Financing Review) / Zawya

- BondbloX

■ アジア・グローバル波及 Asia & Global Spillover

- Nomura Holdings — Asia Macro Analysis

- Institute of International Finance (IIF)

- Institute of Chartered Accountants in England and Wales (ICAEW)

- ASEAN Briefing, Saudi Gazette

■ 法律・規制関連 Legal & Regulatory

- King & Spalding LLP — Saudi Real Estate Reform Analysis

- Latham & Watkins LLP — Saudi Real Estate Law Insights

- White & Case LLP — Saudi Foreign Ownership Law Analysis

- Sovereign Group, Middle East Briefing

本レポートは情報提供のみを目的としており、特定の投資行動を推奨するものではありません。不動産投資にはリスクが伴います。投資判断は専門家にご相談の上、ご自身の責任でお行いください。

This report is for informational purposes only and does not constitute investment advice. Real estate investment involves risks. Investment decisions should be made with professional advice

【ご参考】編集・発行者について / About the Editor & Publisher

塩田 卓也 Takuya Shioda

東京証券取引所プライム市場に上場する不動産デベロッパー、ならびにインフラファンド市場に上場する再生可能エネルギー投資法人において、運用業務に従事してまいりました。

その後は上場企業の経営実務に携わり、不動産開発、産業廃棄物最終処分場事業、エネルギー開発事業を推進。2024年より、中東ドバイおよびサウジアラビアにてアセットマネジメント事業を展開しております。

現在は、日本国内のエネルギー発電所分野と並行し、中東の不動産分野におけるアセットマネジメント事業を軸に活動しております。あわせて、日本の商品・技術・文化を中東市場へ繋げる架け橋となるべく、F&B(飲食)事業への投資や、日本企業の海外進出・貿易支援にも取り組んでおります。

塩田卓也 CEO

EXGROW PROPERTIES LLC・EXGROW INVESTMENT LLC (Dubai / Saudi Arabia)

株式会社EXCEED Energy (Tokyo / Kagoshima)

About the Publisher

I began my career in asset management at a real estate developer listed on the Prime Market of the Tokyo Stock Exchange, and at a renewable energy investment corporation listed on the TSE Infrastructure Fund Market.

I then moved into executive management at listed companies, driving real estate development, industrial waste final-disposal site operations, and energy development projects. Since 2024, I have been developing an asset management business in Dubai and Saudi Arabia.

Today, alongside our power plant business in Japan, our activities center on asset management in Middle East real estate. In parallel, with the aspiration of serving as a bridge connecting Japanese products, technology, and culture to Middle Eastern markets, we are also engaged in F&B investment and in supporting Japanese companies’ overseas expansion and trade.

Takuya Shioda, CEO

EXGROW PROPERTIES LLC・EXGROW INVESTMENT LLC (Dubai / Saudi Arabia)

EXCEED Energy (Tokyo / Kagoshima)